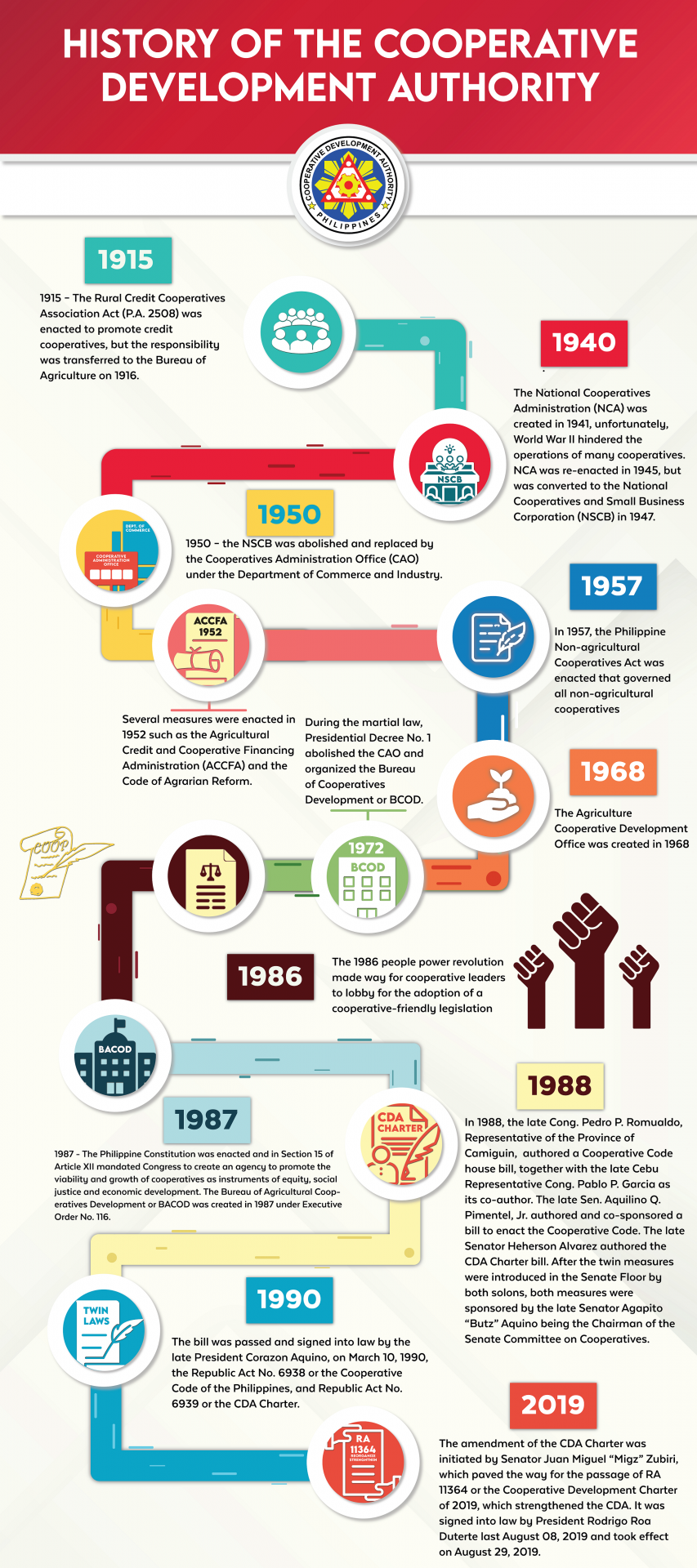

The Cooperative Development Authority (CDA) is a proactive and responsive lead government agency for the promotion of sustained growth and full development of the Philippines cooperatives for them to become broad - based instruments of social justice, equity and balanced national progress.